Schrödinger’s SaaS 🐈⬛ ⁉️

The unhurried take on what's actually changing, sourced from the people closest to it.

“SaaS is dead,” said many with conviction. While others came battling for the opposite view, calling it a panic selloff induced by Wall Street.

We’ve all now learned that the truth is much murkier.

SaaS is, as it happens, simultaneously under threat — and it would be irresponsible to think otherwise. But also still deeply entrenched, and it would be equally irresponsible to “project a 5-person startup behavior onto a Fortune 500” in the words of Sarah Guo from Conviction.

A moment that renders itself perfectly to Schrödinger’s uncanny experiment.

We wanted to dedicate this edition to the nuanced takes from the interwebz that carry the rigor this moment, uncanny as it is, warrants.

Let’s start with what has fundamentally shifted, the thing that led to all of this speculation and chaos: AI has made the SaaS business model unstable.

SaaS margins were anomalously high, in most part because of three factors — zero marginal cost of reproduction, non-ephemeral value, and high switching costs. AI degrades all of them simultaneously: inference adds real cost, faster model cycles accelerate depreciation, and agents don’t particularly care which tool they’re using.

On top of that, the abundance of code can threaten pricing power, a pure-play seat-based model can have serious limitations when charging for work, and the model companies themselves can double-up as very capable competition, almost out of the blue.

The extent of the selloff was dramatic, yes, but the market pressure on public SaaS does have some feet. Avenir’s January 2026 report shows that public SaaS companies have not been performing as well as they used to. At this point 2020-21 seems like an aberration:

Public SaaS median revenue growth, peak (Q2 2021): 44%

Public SaaS median revenue growth, Q3 2025: 18%

SaaS equity performance since Nov 2021: -27%

Horizontal SaaS index since Nov 2021: -49%

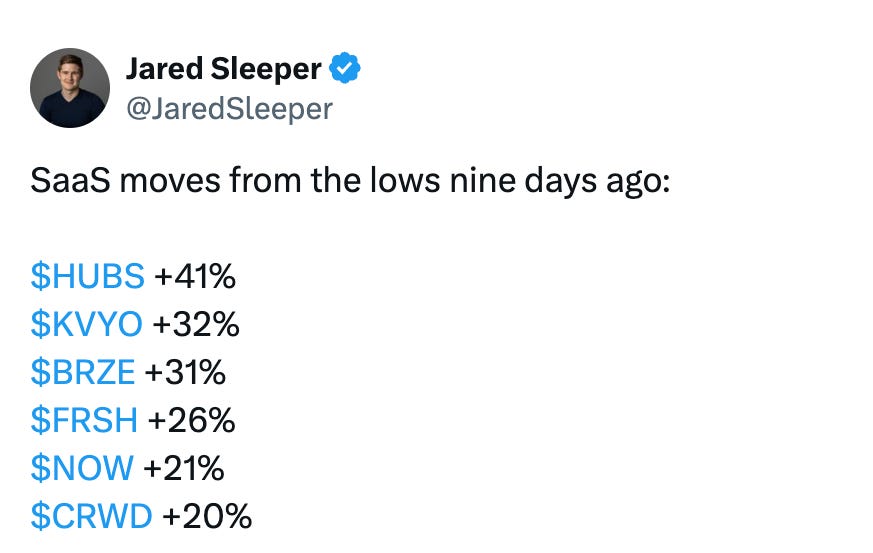

Interestingly, a cool-off post the much hotly debated sell-off is already afoot.

The public markets have shown that they were, and will continue to be, swayed by incentivized narratives, poorly-informed fears, and short-term hedging. The builders need to focus on an entirely different set of questions. Let’s dive in:

#1. The threat from the model makers

It’s no coincidence that the selloff came right after Claude launched plugins for 11 use cases like marketing, legal, and sales. When the model maker shipped something that could be even a bit of the interface, every company that owned it was asked to defend itself.

Elad Gil on No Priors points to a historical pattern here: Microsoft forward-integrated into Office, Google forward-integrated into vertical search — travel, local, maps. The AI labs will likely do the same.

Elad shared that every major platform shift has seen the platform move into the most valuable applications sitting on top of it. The question he raises for every founder is: “which verticals are durable and defensible, and which ones will get eaten?”

There are three popular ways companies are navigating this — each with a different logic:

1. Own institutional judgment, not just the interface

On February 3, Anthropic released the Claude Cowork legal plugin and Thomson Reuters dropped 16–18%. Three weeks later, at a separate Anthropic enterprise event, Thomson Reuters’ CoCounsel AI tool was featured on stage and CEO Steve Hasker presented.

The stock surged 11–14% that day, its biggest intraday gain in 26 years. Hasker’s argument was that Anthropic builds good general-purpose automation, but replicating what Thomson Reuters offers would require massive investment to acquire decades of curated legal content and 2,700+ attorney editors.

Rajan frames this as the real moat: the density of institutional knowledge encoded in how your humans and agents work together. That can’t be made a feature or a plugin.

2. Specialize into what’s too specific/niche for a foundation model to bother

Spellbook, a contract drafting tool for lawyers, found that the Claude legal plugin launch actually increased their usage. Their take is that a foundation model will automate the generic user cases. It won’t go deep enough into the focused workflows, edge cases, and jurisdictional nuances that a specialized tool has spent years encoding.

As the analogy goes — every startup used to be asked why Google wouldn’t kill them and the answer has simply been the fact that those areas are just too niche or too specific to be worth it for them.

3. Build in a way where every model improvement makes you better, not obsolete

Crosby, an AI legal services company, started with lawyers in the loop — deliberately. Their reasoning: “You want to do end-to-end work, what you’d expect from a law firm. AI can’t do this alone.” Their bet is that by encoding legal judgment alongside AI capabilities, each improvement in the underlying model makes their product better rather than threatening it.

#2. Worse than SaaS. Better than most everything else.

“Software is a business tool, not a business model.” — Sam Lessin

Software was always a tool. It was SaaS that was the business model, of a certain outperforming shape. And now that shape is changing.

Dave Kellogg of Balderton Capital predicts the Rule of 40 becomes the Rule of 60 in this podcast conversation, as margins compress and AI raises the cost of delivery, the threshold for a compelling SaaS business rises.

This transition is yet to be realized fully, and one of the levers that will play into it the most will be the monetization model, which has dominantly been seat-based.

For instance, GitLab is one of the companies that has benefited tremendously from AI wrt an uptick in usage/adoption, but their pricing is making them leave money on the table. The GitLab CEO Bill Staples and CFO Jessica Ross hinted at the importance and urgency for a need for pricing innovation during the Morgan Stanley TMT conference. They shared:

“Their current business model of seat-based pricing didn’t anticipate the surge in AI-driven surge in platform usage. Customers get unlimited access per seat which means the business has delivered more value without capturing more revenue.”

The pricing shakeup will be uncomfortable in the short-run but will ultimately be the only way to keep and grow margins in proportion to the value delivered. And based on what we’ve seen work and break while enabling companies make this transition, we’d add a +1 to the urgency that pricing innovation warrants.

Margins will still exist, they will just be compressed. A pure software business that earned 25% income margins might earn 10–11% going forward. Yoni Rechtman calls this in his post “Creating margins after SaaS.”

“The income statements will look ‘worse’ by SaaS standards and better by every other standard. The software companies that succeed in this brave new world won’t be pure application software and they certainly won’t be traditional SaaS. But they will be bigger and throw off huge amounts of cash to their shareholders — at permanently lower margins.” — Yoni Rechtman

Lower margins don’t automatically mean bad businesses. The question is whether the company can still generate durable value. Rechtman considers three potential paths:

Network effects — Value that compounds with scale, cost to compete that rises with each new participant. Agents interacting with your network accelerate the compounding.

Sin eater — Absorbing high-stakes, operationally intensive work that businesses want off their plate. Security, fintech, compliance, legal. Too high-volume to do manually, too high-stakes to do generically. That’s durable.

Hybrid models — Software plus services, hardware plus software. Physical switching costs, proprietary data from sensors and devices, forward-deployed humans. This is why Samsara is holding up when pure horizontal SaaS isn’t.

“Connecting the foundation models to high value complex real-world use cases is the biggest opportunity for wealth creation in recent memory. It will happen through new (often hybrid) business models and products rather than re-running the cloud playbook.” — Yoni Rechtman

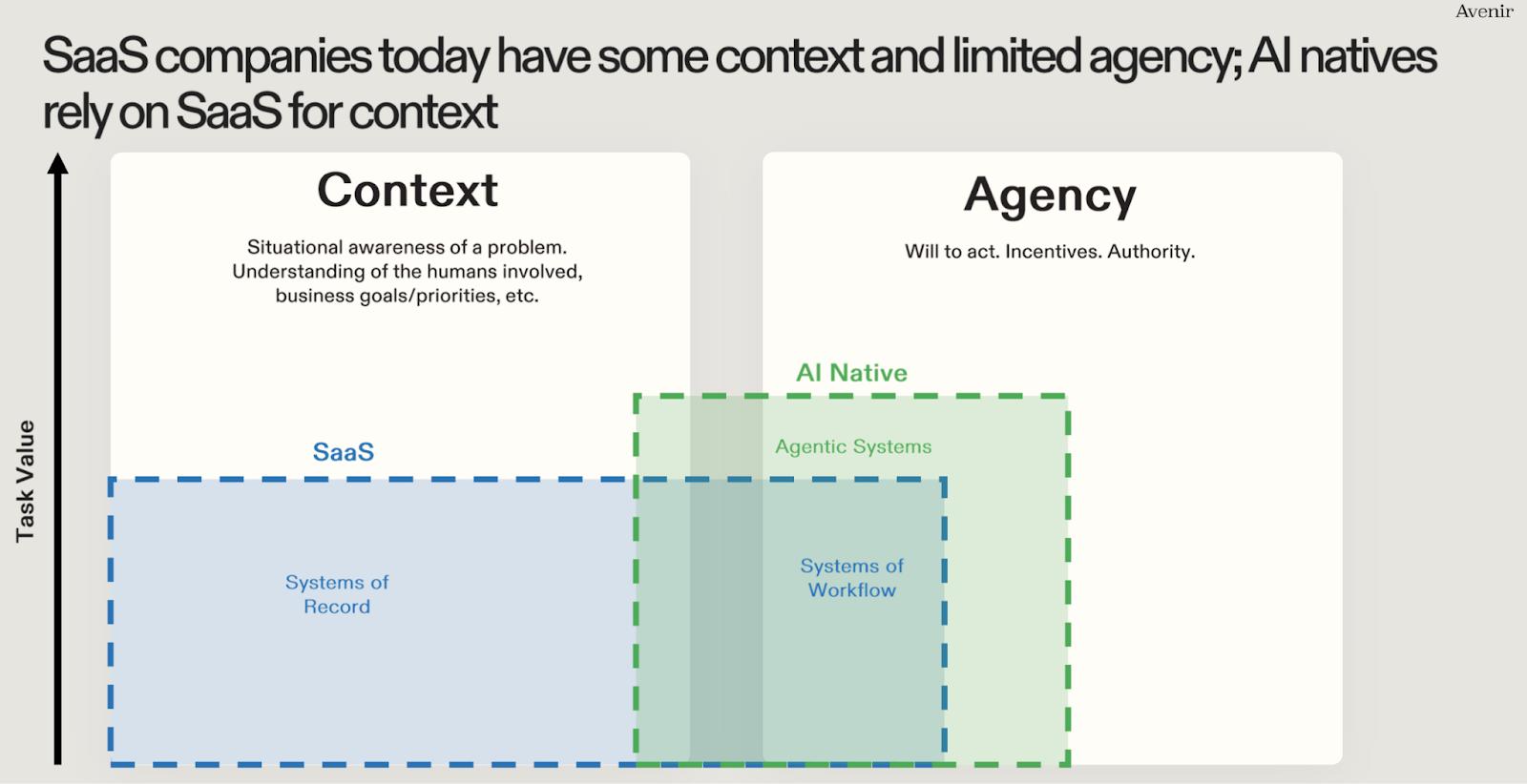

#3. The next battle is for context

Another useful idea from Avenir’s January 2026 deck is the fast-intensifying battle for becoming a system of context which is playing out across enterprise categories.

Intelligence is commoditizing fast, GPT-4 level capability dropped from $60 to $0.40 per million tokens, a 99% reduction. What doesn’t commoditize is context: situational awareness of a problem, knowledge of the humans involved, institutional operating norms.

Some incumbents are winning the early agentic revenue: Intercom’s Fin at $100M+ ARR, Salesforce Agentforce at $540M ARR, ServiceNow Now Assist at $500M+ ARR. What’s worth noting is that these wins are concentrated in the support and service workflow category. Re: the AI-natives, they are building fast, but without the context advantage yet.

Emphasis on yet.

Further, only 2–7% of enterprise buyers put more than 80% odds on replacing major vendors like Atlassian, Workday, or Salesforce in the next five years. Systems of record aren’t being ripped out en masse. But the interface layer above those systems, and the workflow layer between them, is actively being contested.

Atlan’s co-founder, Prukalpa Sankar, shares why things are going to get complicated for both sides of the battle: “context is cross-system, multilayered, and heterogeneous”. Every enterprise has a different combination of tools; one runs Salesforce + Zendesk + Snowflake, another runs something else entirely. She goes on to illustrate why:

A renewal agent, for example, doesn’t just pull from your CRM. It needs PagerDuty, Zendesk, Slack, Salesforce, and Snowflake to do its job. To truly capture the context graph, a vertical AI startup would need to integrate 50–100+ systems just to cover common cases. Incumbents represent one part of the stack. AI natives have to figure out the whole thing.

Theory Ventures’ GP (and backer of 9 enterprise unicorns!), Tomasz Tunguz, adds another dimension to the context battle: incumbents are already changing the rules of the game. Salesforce restricted Slack’s API, Datadog deactivated a competitor’s account, and Epic faced a lawsuit for gatekeeping patient records. If your architecture depends on clean programmatic access to incumbent data, plan for that access to get more expensive or disappear.

He foresees that some AI products will make such defensive attempts futile by changing the very internal processes that SORs serve today:

“When AI products are sold as services, they replace in-house labor. This changes internal processes. When the internal processes change, the opportunity to replace the system of record arises because the existing workflows are no longer relevant.”

#4. In the age of abundance, who wins?

“If code, compute, and intelligence are all getting cheaper — who actually wins?”

Packy McCormick grounds all the different facets, opportunities, hype, et al. with this one question. He then turns to history to gather what has worked in domains that have seen similar abundance of inputs.

Looking at Rockefeller, Carnegie, Swift, and Ford, he highlights the playbook they all ran: identifying the binding constraint holding an industry back, breaking it using new technology, seizing the resulting High Ground, and integrating outward from there.

“…what matters is becoming the leader in your industry in a way that is incredibly specific to that industry and in such a way that your business benefits from, instead of being threatened by, abundant improvements in general purpose technologies like AI and batteries.”

Packy adds a unique, helpful nomenclature: “The High Ground is the scarce and valuable position you win by breaking it. Moats are what keep others from taking it.”

Ramp vs. Brex makes it concrete for our world of SaaS. Ramp is worth $32B. Brex sold to Capital One for $5.15B. Not because of a 6x revenue difference, but because of something else. In Packy’s words here’s what happened:

“Ramp used a card, software, and counter-positioning to attack what it viewed as the Schwerpunkt in corporate spend (the fact that everyone was selling money, and no one was selling time) and win the transaction layer, the High Ground from which it is now expanding to eat every point solution a finance team touches.”

In this same post, Packy shared Flexport’s Ryan Petersen tweet putting it plainly: “We’re so lucky we didn’t listen to all the people who told us to be SaaS — almost everyone ‘smart,’ by the way.” He was advised to sell software to freight forwarders rather than actually becoming a freight forwarder and competing. Flexport became the freight forwarder.

He shares an equally pointed implication for investors:

“…getting comfortable with a wider range of business models to accommodate whichever is the right one for the industry in which a company operates. This does not mean that they should treat all business models equally now. Instead, they need to stop blind pattern matching altogether.”

He goes on to add that services businesses might be terrible for most companies but exactly right for some. Stripe shouldn’t be a services business. An AI-native law firm probably should be.

#5. Vibe coding as a threat, or not

The loudest version of the bear case goes like this: AI makes software so easy to build that companies will just vibe-code their own tools internally, collapsing demand for SaaS entirely.

It’s a good story. It’s not what’s actually happening.

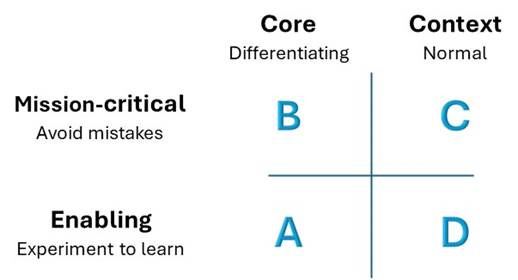

Geoffrey Moore — three decades advising Salesforce, Microsoft, and SAP — makes the structural argument. He says that every enterprise activity is either Core (what differentiates the company) or Context (everything else — regulatory compliance, standard operations). Mission-critical context is where SaaS lives. And it should never be differentiated. You’d want payroll to be reliable, auditable, and maintained by specialists whose entire business is exactly this problem.

He adds:

“Could you use AI to write your own system of record? Yes, you could. But why? Advocates will say it will save you money — is that really true? In year one, it is. But before you declare victory, ask yourself how realistic your DIY accounting is, especially if you have neglected to incorporate annual maintenance, not to mention a discount for risk, and another discount for the opportunity cost of distracting your AI talent from pursuing core.”

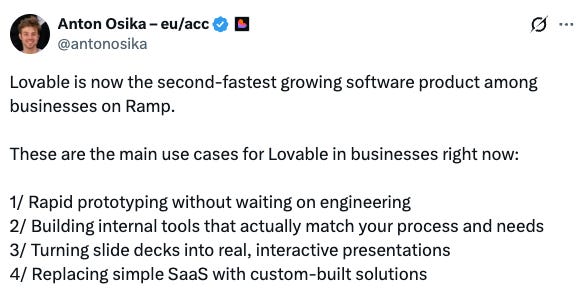

The heart of Geoffrey’s statement is in the examples he states — a system of record, an accounting platform… the complex stuff — leaving a very specific tail-end of simple SaaS apps exposed, and a recent analysis by Anton Osika of Lovable validates it:

Jason Lemkin from SaaStr shared his perspective on what’s happening:

“People aren’t vibe coding their own Salesforce. They’re not rebuilding Workday or replacing Snowflake. They’re replacing the $49/month SaaS tool that does 80% of what they need and 40% of what they don’t.

Simple B2B apps. Simple ones…This is meaningful for B2B founders to pay attention to. The “simple tool” end of the market is going to get compressed.”

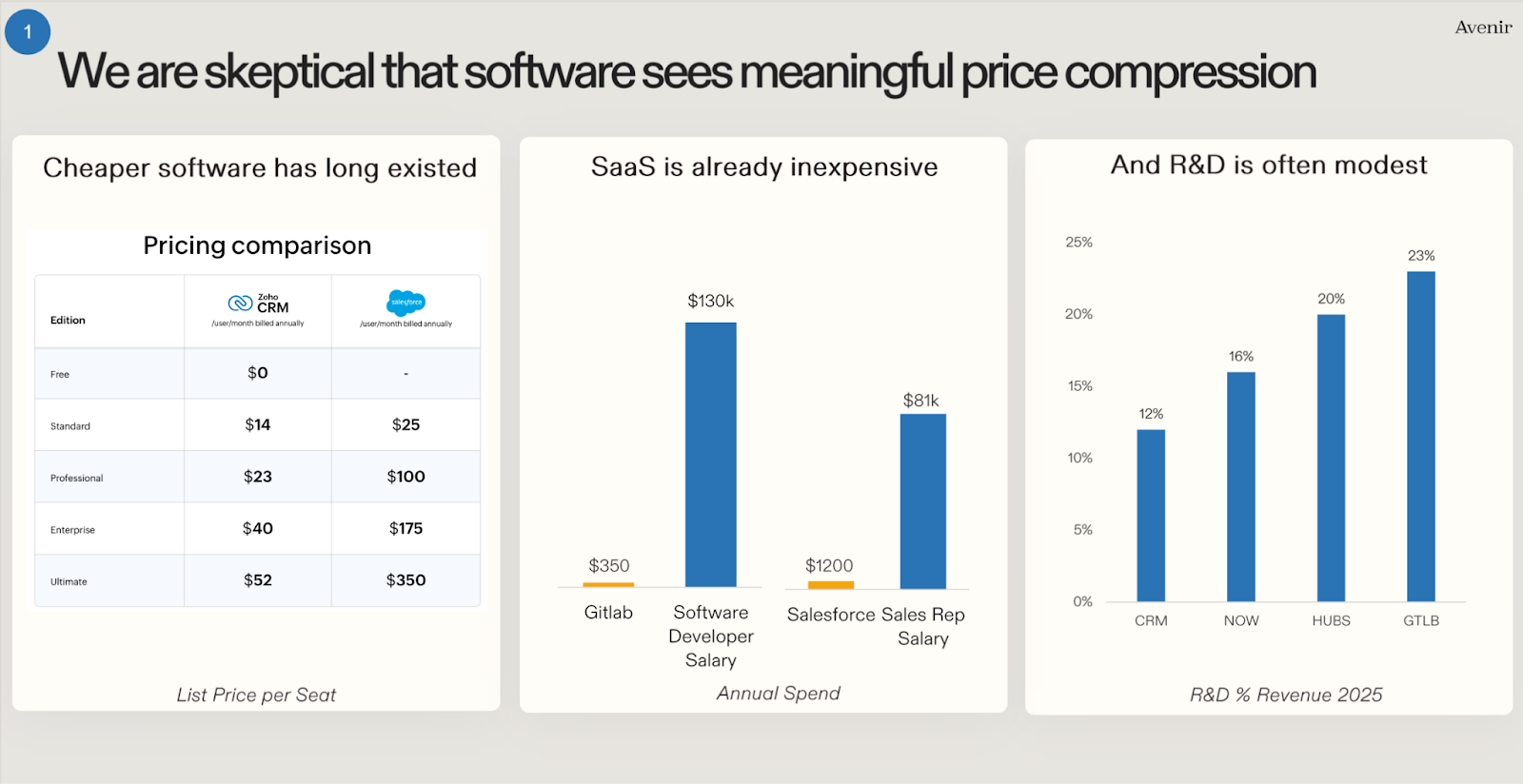

For the platforms and the complex tools, Avenir’s data closes the loop with a throwback insight on price compression. Cheaper software has always existed. Zoho has undercut Salesforce for two decades without meaningfully compressing SaaS pricing.

SaaS is already inexpensive relative to the labor it replaces, a Salesforce seat at $1,200/year versus an $81K sales rep salary. And R&D as a percentage of revenue is often modest, meaning there’s less cost advantage to building in-house than it appears.

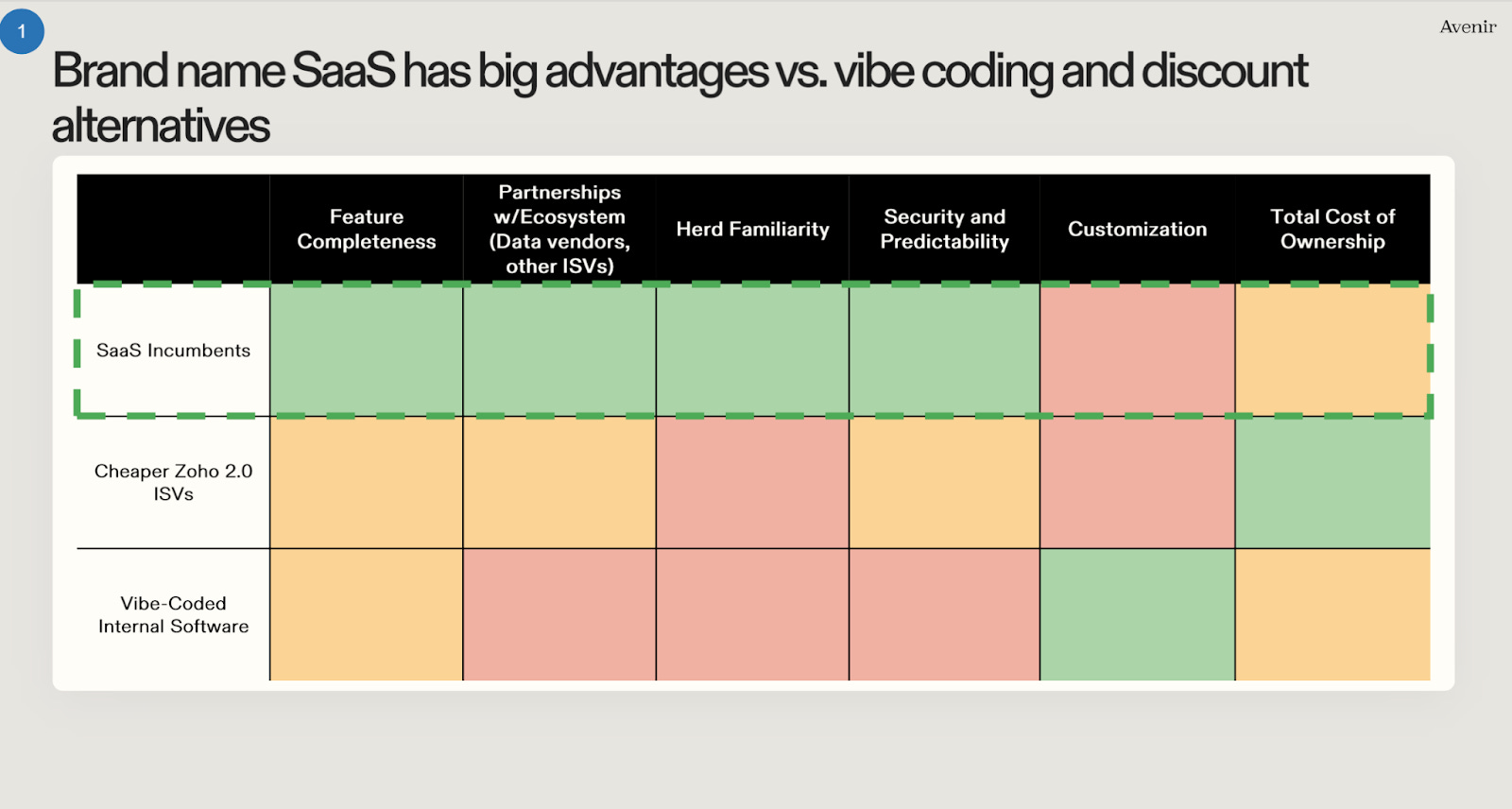

Further, brand-name SaaS offers more than code. They win on feature completeness, ecosystem partnerships, security, predictability, and herd familiarity. Vibe-coded alternatives win on customization and cost, two dimensions that matter less for mission-critical workflows.

#6. The timeline and the horizon

The honest version of the bear case isn’t “everything disappears overnight.” It’s that the unit economics of pure application software have structurally changed, and the market won’t pay 2021 multiples for that profile again. Less dramatic than the discourse, but more accurate.

Rory O'Driscoll captures this shift succinctly:

“There are growth investors and there are value investors, and there is a chasm in between. The SaaSpocalypse is really about the SaaS story shifting from the former to the latter.

From 2004 to 2019, public SaaS companies grew at an average of 30% and were valued at an average of 6x revenues. It was the best, most predictable growth story in the market. Then two years of COVID gave us 40% growth at 20x revenues.

…Everyone is finally realizing that the growth story is all AI. SaaS companies without AI-driven growth will be valued like every other company in the market, on a growth adjusted multiple of free cash flow. Amazing companies with real value but no pixie dust premium.”

That’s what it is, the pixie dust premium has settled.

Sources: MT Rajan · Yoni Rechtman · Dan Hockenmaier · Avenir · Geoffrey Moore · Packy McCormick · No Priors · Jamin Ball · Jason Lemkin · Prukalpa Sankar · Tomasz Tunguz · Rory O’Driscoll

PMF /evals ◎ is just getting started. Tell us about how you’re approaching AI-native building in the wild! Or what you’d like us to cover. Hit reply.